This article originally appeared in the Sound Advisory blog. Sound Advisory provides financial advisory services and specializes in educating and guiding clients to thrive financially in a bitcoin-powered world. Click here to learn more.

One of the simplest and most effective ways to improve your financial situation: Don’t get killed on taxes.

Taxes are a major friction in most people’s financial lives, and a little foresight and planning can go a long way. This article will cover a few helpful tips and case studies that could help you improve your future tax planning.

Let’s touch on a quick refresher. Keep these two foundational concepts in mind as you consider possible strategies.

Cost basis: Keep detailed records of all your bitcoin transactions

Maintaining meticulous records of every bitcoin transaction and its associated cost basis is not just a good practice but a crucial one, given the Internal Revenue Service’s (IRS) authority to audit returns up to six years back.

The answer is yes if you’re wondering whether the IRS can track bitcoin transactions. The IRS employs various means to monitor bitcoin activities. Here’s how:

- KYC Compliance: All major cryptocurrency exchanges must conduct Know Your Customer (KYC) checks, ensuring that your identity is tied to your holdings.

- Transaction History: Many exchanges keep detailed records of the addresses associated with your withdrawals. This enables them to identify custodial wallets and track additional downstream transactions.

- Reporting to IRS: Numerous exchanges must submit 1099 forms to users and the IRS, providing a comprehensive overview of taxable events and gains.

- Legal Precedents: The IRS has successfully litigated cases against prominent exchanges such as Coinbase, Kraken, and Poloniex, compelling them to disclose customer data. This legal standing solidifies the IRS’s ability to access crucial information about bitcoin holdings and transactions.

Given these measures, it is essential to recognize that the IRS is well-informed about bitcoin activities. Consequently, it is prudent to strategize your bitcoin tax plan accordingly.

Many individuals venture into bitcoin investments without fully grasping the potential tax implications. Buying, selling, trading alternative coins, and switching exchanges may seem routine, but each event carries distinct tax implications. Neglecting these consequences can result in a complex situation during tax season.

To navigate the intricacies of bitcoin taxation, it is imperative to establish and comprehend your cost basis. Taking the time to go back and organize your past transactions and maintaining clear, systematic records moving forward can streamline the tax reporting process, saving you time and mitigating potential issues. If you find the landscape of bitcoin taxes overwhelming, seeking guidance from a tax professional is a wise step to ensure that you are well-prepared and in compliance with tax obligations related to your bitcoin investments.

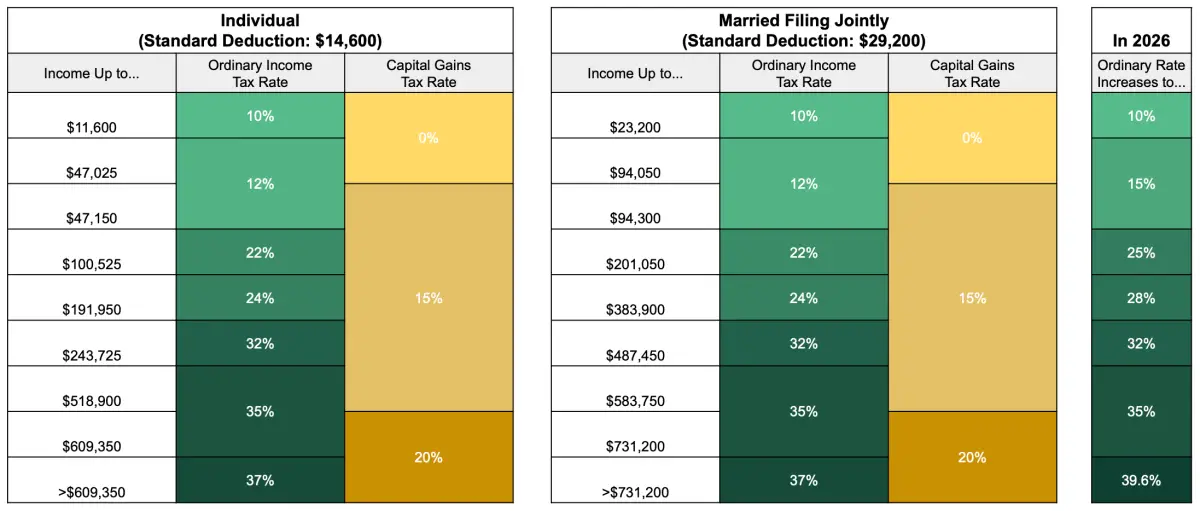

Tax tables: Not all bitcoin is taxed the same

The IRS treats bitcoin as property, not money, so it is subject to capital gains tax (not ordinary income tax) when sold, traded, or spent. Capital gains are taxed under two possible taxation tables: short-term and long-term capital gains.

The following table helps visualize: Short-term gains on bitcoin held one year or less are taxed as ordinary income rates (green column). Refer to the yellow column if bitcoin is held for more than a year.

If you hold bitcoin for over a year before disposing of it, you will pay long-term capital gains tax, which ranges from 0% to 20%, depending on your income.

Furthermore, these tables only apply to non-qualified bitcoin—bitcoin not held in a retirement account. Qualified distributions from Traditional IRA bitcoin are always taxed as ordinary income (green), and Roth IRA distributions can be tax-free.

With that as a backdrop, let’s get into some potential strategies that many bitcoiners often overlook.

Strategies and Case Studies

Bitcoin tax can snowball: Evaluate your cost-basis strategy

Purchasing bitcoin is like freshly fallen snow – pure and untouched. It isn’t taxable. But you incur a taxable event when you set foot in that snow with a sell, trade, or spend. And similar to how a snowball grows as you roll it down a hill, the tax implications of your bitcoin transactions can accumulate over time.

When accounting for transactions, it’s important to remember that each event will impact your cost basis.

The IRS allows for “specific identification” accounting for bitcoin, where you keep track of every inventory item—in this case, every chunk of bitcoin. Specific identification has variations like FIFO (first-in, first-out), LIFO (last-in, first-out), and HIFO (highest-in, first-out) when matching dispositions (sells, trades, spends) with acquisitions (buys, income). With a good identification record, you can run projections to see which method gives you the lowest gains.

Scenario: Adam bought 1 BTC in January 2023 for $16,000 and another 2 BTC in March 2023 for $48,000. He sold 1 BTC in August 2023, when 1 BTC is worth $30,000.

- With FIFO, Adam has a $14,000 capital gain (sale price of $30,000 less cost basis of $16,000).

- With LIFO, Adam has a $6,000 capital gain (sale price of $30,000 less cost basis of $24,000).

- HIFO is the same as LIFO in this case.

These would be short-term capital gains, so let’s assume a hypothetical 22% federal tax rate. Adam can pay $1,760 less tax by choosing LIFO over FIFO.

It’s quite simple when there are only a few transactions, but it can easily become complicated with every additional buy, sell, or spend. Cost basis and the subsequent transaction matching is an evolving calculation that could have drastic consequences if done incorrectly.

Tax loss harvesting

Recently, bitcoin has been trading near its all-time highs. So, this strategy is less relevant, but we’ll leave it here for future readers.

In a tax loss harvesting strategy, you can sell at a loss to offset other income or capital gains and lower your tax liability. If you have realized capital gains from selling bitcoin this year, look at coins you’re still holding that are trading below their purchase price.

Scenario: Hal has a $15,000 short-term gain from selling a stock before holding onto it for a year. In December, he decides to sell some bitcoin at a $12,000 loss. This offsets $12,000 of his stock gain, so he only needs to pay capital gains tax on the remaining $3,000 gain instead of $15,000. At a 22% tax rate, $2,640 is saved.

Just because you had a loss this year doesn’t mean you necessarily want to use that loss this year. You can look at using the tax loss carry forward technique. Up to $3,000 in annual losses can offset your other income (things like wages, rental income, etc.). However, any amount over $3,000 must be carried forward to be used in future years. Some strategic clients may decide to harvest and report losses now so you can reduce taxes and carry them forward to offset future gains.

If attempting to harvest losses, please be aware of the wash sale rule, described in further detail at the end of this article.

Tax gain harvesting: The 0% tax bracket

A peculiar tax rate in the capital gains table above is 0.00% tax on long-term capital gains.

For 2024, if total taxable income falls under $94,050 as a married couple ($47,025 single), you can sell long-term capital assets, and gains are taxed at 0% federally. Paying a 0% tax ain’t so bad. Sign me up. I’ll even pay it twice.

And “taxable income” is calculated after the standard deduction, which adds another $29,200 for married ($14,600 single).

Scenario: Let’s assume Stacey and Max are married with $100,000 combined in W2 income from their jobs at the embassy. They sell some bitcoin throughout the year and realize a $16,000 long-term capital gain. Some quick math: $100,000 (W2) plus $16,000 (cap gain) is $116,000. Take out the standard deduction of $29,200, and the taxable income is $86,800. Since their total taxable income for the year is below the $94,050 threshold, their bitcoin gains are taxed at 0% (tax-free). And we’ll assume that they live in one of the nine US states that don’t have an income tax, so let’s call it 0% state tax as well.

It is possible to sell non-retirement bitcoin tax-free—valuable information for those looking to sell. If you are in a situation where you think these income levels/brackets may apply to you (now or in the future), a strategic sell and immediate rebuy opportunity awaits: the tax gain harvest.

Sometimes, it makes sense to sell bitcoin, recognize a gain at 0% rates, and immediately buy it right back. By repurchasing the bitcoin immediately, you effectively set a new cost basis for your investment. This new basis is higher than your original purchase price. In the future, if bitcoin’s value continues to rise and you decide to sell again, you’ll be taxed on a smaller gain, thanks to the earlier gains harvesting.

Gains harvesting is: sell your bitcoin, take advantage of the 0% bracket, and buy it right back (wash sale rules only disallow losses – not gains).

The desired outcome here is an increase in tax basis. In the future, you’ll be taxed on a smaller future gain, thanks to the earlier gains harvesting.

A prime opportunity for gains harvesting often comes during retirement. When people stop working, they typically stop receiving income from their jobs (say goodbye to those W2s!). This significant drop in income could place them in that coveted 0% tax bracket. With that extra room, they can maximize their tax strategies not just with gains harvesting but also with other income structuring strategies Roth IRA conversions or liquidating assets through installment sales.

Gifting

We’ll cover three target gift recipients: charitable organizations, donor-advised funds, and other people.

Charity

When you donate bitcoin to a qualifying charitable organization, you can deduct the full fair market value of the donation. This will allow you to avoid paying capital gains tax on the appreciation before gifting yet still get the write-off. Donating bitcoin directly rather than cash proceeds from selling it is more advantageous, as the latter would trigger capital gains tax. Just remember to obtain a receipt from the charity for your records and get a special valuation assessment if needed.

Scenario: Jack bought 1 bitcoin in 2015 for $200. It’s now worth $70,000. He donated 0.25 BTC to a charity this December and got a receipt showing its value of $17,500. Jack claims a $17,500 charitable deduction. If he had sold the bitcoin and given cash instead, he’d pay tax on $17,450 in capital gains.

You can effectively give more value by gifting rather than selling and giving cash.

“But I don’t want to have less bitcoin!”

If bitcoin holders are familiar with “spend and replace,” we can consider a similar strategy like “donate and replace.” You can gift appreciated bitcoin and repurchase with cash to increase the cost basis (like the above example – gains harvesting), thus lowering future taxes.

Donor-advised funds

For regular or substantial contributors to charitable causes, a donor-advised fund (DAF) presents a mechanism for amplifying their philanthropy. Think of a DAF as a “charitable savings account”: You make contributions with assets, secure an immediate tax benefit, and then, at your discretion, advise on investing those assets and distributing the grants to charities of your choice over time.

Incorporating bitcoin into this structure introduces an exciting dynamic. Given its potential for significant appreciation, designating it as an asset within a DAF can exponentially magnify the fund’s growth potential. The result? A larger reservoir of resources dedicated to driving positive change in the world, all while efficiently navigating tax implications.

Friends and family

Giving bitcoin to others transfers the original tax basis and gets bitcoin out of the estate.

Instead of selling bitcoin and realizing gains, you can gift bitcoin up to the annual gift exclusion amount of $18,000 per person per recipient. The gift tax annual exclusion is the amount you may give each year to individuals and certain types of trusts tax-free without using any of your gift and estate tax exemption. As the giver, you do not owe taxes on gifts under the exclusion amount of $18,000. The recipient inherits your cost basis and will owe capital gains when they eventually sell (perhaps at a lower bracket/rate than you).

Scenario: A married couple, the Nakamotos, want to give a significant amount of bitcoin to their daughter Kristina and her new husband. Annual exclusion amounts are $18,000 per person. Effectively, the Nakamotos can gift $72,000 without dipping into their “lifetime bucket.” Dad to Kristina. Dad to husband. Mom to Kristina. Mom to husband. $18,000 each.

Roth accounts

Using a Roth IRA can eliminate ALL future tax liability.

If eligible, contributing to a Roth IRA or 401k allows for tax-free appreciation and distribution if held to age 59.5. Since Roth accounts provide tax-free growth, they are ideal for long-term bitcoin holdings.

If you own bitcoin outside an IRA that you want to hold long term, you could sell the bitcoin, contribute the USD proceeds to the Roth IRA, and repurchase the bitcoin inside the Roth. This eliminates the bitcoin cost-basis tracking requirement and allows future appreciation to be tax-free upon qualified distribution.

Conclusion

The maximum contribution to an IRA in 2024 is $7,000 per person ($8,000 if over 50), and you have until April 2025 to make 2024 contributions. Consult your financial or tax advisor to see if this strategy suits you.

With proper tax planning, bitcoin investors can maximize after-tax returns and minimize tax liability. Work closely with your tax professional to implement the right strategies based on your situation. Keep meticulous records and understand the nuances around cost basis, tax loss harvesting, retirement accounts, charitable gifting, and other techniques. The bitcoin tax rules can be complex, but the long-term rewards of proper planning are well worth the effort.

A note on wash sales

The wash sale rule prevents claiming a capital loss if you repurchase the same security within 30 days before or after the sale. This rule currently applies only to securities, not commodities like bitcoin.

Some bitcoin investors have taken advantage of this loophole by selling at a loss and immediately repurchasing while claiming the capital loss to reduce their tax liability. This tax loss harvesting strategy is extremely risky and not recommended.

Even though wash sales are not explicitly prohibited for bitcoin yet, the IRS could determine this pattern violates the essence of wash sale rules under the step transaction doctrine. Engaging in systematic wash sales to harvest losses could trigger penalties and interest if identified in an audit.

It is safer to avoid wash sales of bitcoin, even though technically allowed now. Do not sell at a loss and reacquire the same bitcoin within 30 days before or after the sale. Consult a qualified tax advisor before attempting any tax strategies involving cryptocurrency.

1) Transferring bitcoin between your wallets is not taxable. Only transfers between separate parties are taxable events.

2) These rates only affect federal taxation. Capital gains are taxed in varying ways and rates at the state level. Please consult your tax professional regarding state taxation, as it may change the appropriate strategies and recommendations for your situation.

CONTACT

Office: (208)-254-0142

408 South Eagle Rd.

Ste. 205

Eagle, ID 83616

hello@thesoundadvisory.com

Check the background of your financial professional on FINRA’s BrokerCheck. The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. Please consult legal or tax professionals for specific information regarding your individual situation. Some of this material was developed and produced by FMG Suite to provide information on a topic that may be of interest. FMG Suite is not affiliated with the named representative, broker – dealer, state – or SEC – registered investment advisory firm. The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

We take protecting your data and privacy very seriously. As of January 1, 2020 the California Consumer Privacy Act (CCPA) suggests the following link as an extra measure to safeguard your data: Do not sell my personal information.

Copyright 2024 FMG Suite.

Sound Advisory, LLC (“SA”) is a registered investment advisor offering advisory services in the State of Idaho and in other jurisdictions where exempt. Registration does not imply a certain level of skill or training. The information on this site is not intended as tax, accounting, or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. This information should not be relied upon as the sole factor in an investment-making decision. Past performance is no indication of future results. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. It should not be assumed that any recommendations made will be profitable or equal any performance noted on this site.

The information on this site is provided “AS IS” and without warranties of any kind, either express or implied. To the fullest extent permissible pursuant to applicable laws, Sound Advisory LLC disclaims all warranties, express or implied, including, but not limited to, implied warranties of merchantability, non-infringement, and suitability for a particular purpose.SA does not warrant that the information on this site will be free from error. Your use of the information is at your sole risk. Under no circumstances shall SA be liable for any direct, indirect, special or consequential damages that result from the use of, or the inability to use, the information provided on this site, even if SA or an SA authorized representative has been advised of the possibility of such damages. Information contained on this site should not be considered a solicitation to buy, an offer to sell, or a recommendation of any security in any jurisdiction where such offer, solicitation, or recommendation would be unlawful or unauthorized.